Tips for Single Homebuyers: How To Make Your Dream a Reality

If you’re living on your own and looking to buy a home, know that you can make your dream a reality with thoughtful planning and the right team of experts. Research from Freddie Mac shows 28% of all households (36.1 million) are sole-person, and that number is growing. Over the past 40 years, the number of sole-person households has nearly doubled, and that’s a trend that’s expected to continue. According to Freddie Mac:

“Our calculation suggests that there will be an additional 5 million sole-person households in the United States by the next decade. This means 42% of the household growth will be contributed by sole-person households, . . .”

If you fall into this category, here are three tips to help you achieve your homeownership goals.

1. Know Your Credit Score

When you buy a home on your own, you have to qualify for your loan based solely on your own finances and credit history. Investopedia says:

“. . . lenders will be looking at just one credit profile: yours. Needless to say, it has to be in great shape. It is always a good idea to review your credit report beforehand, and this is especially true of solo buyers.”

It’s important to find out your score so you know where it falls. If you’re not sure if it’s strong enough or where to focus your energy to improve it, meet with a professional for expert advice on your individual situation.

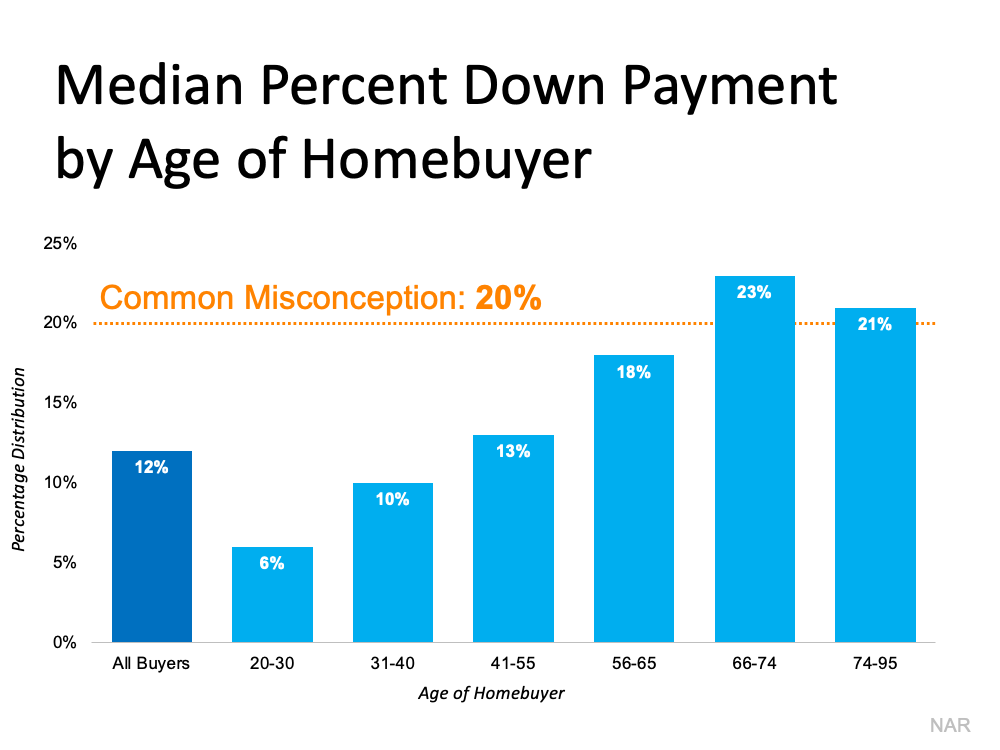

2. Explore Down Payment Options

Next, look into down payment programs so you can get a feel for what you’ll need to save to buy a home. Rob Chrane, CEO of Down Payment Resource, explains:

“Buyers should discuss their program options with their loan officer and real estate agent to make sure they choose the program best suited to their personal needs.”

In this step, lean on the pros to determine what you’re eligible for and what’s right for you.

3. Think About Your Future Home and Your Needs

You should also spend time thinking about what you want. What type of home do you picture yourself in? To answer that question, Quicken Loans shares this advice:

“Think about your lifestyle, what you want out of your home and your needs. Is being close to work important? Do you need a lot of yard space? Do you want an extra bedroom that you can transform into a home office? Condo or detached home? Lots of space for entertaining? It’s all up to you (and your budget).”

Again, a professional can help you balance what you want and how much you should spend on your monthly housing costs to determine what type of home is right for you.

While buying a home solo can feel like a big challenge, it doesn’t have to be. If you lean on the professionals, they can help you navigate these waters and make sure you’re able to take advantage of the great opportunities in today’s housing market (like low mortgage rates) to buy your dream home.

Bottom Line

The share of sole-person households is growing. If you’re looking to buy a home on your own, be confident that the dream is achievable. When you’re ready to begin your search, let’s connect so you have expert advice each step of the way.

|

|

|

JERRY TORRES’

Sr. Mortgage Loan Originator #TechieLoanOriginator | #JerryTorresPro

Prime & NON-Prime Home Loans | Bank Statement Loans | ITIN | HELOCs |

![Fact or Fiction: Homebuyer Edition [INFOGRAPHIC] | Simplifying The Market](https://www.jerrytorres.pro/blog/wp-content/uploads/2021/09/20210910-MEM.png)