How Your Tax Refund Can Move You Toward Homeownership This Year

If you’re looking to buy a home in 2020, have you thought about putting your tax refund toward a down payment? Homeownership may be one step closer than you think if you spend your dollars wisely this year.

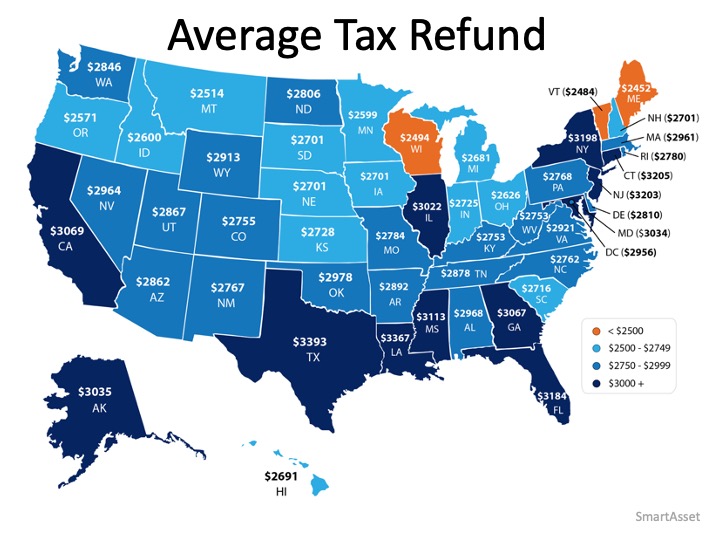

Based on data released by the Internal Revenue Service (IRS), Americans can expect an estimated average refund of $2,962 when filing their taxes this year.

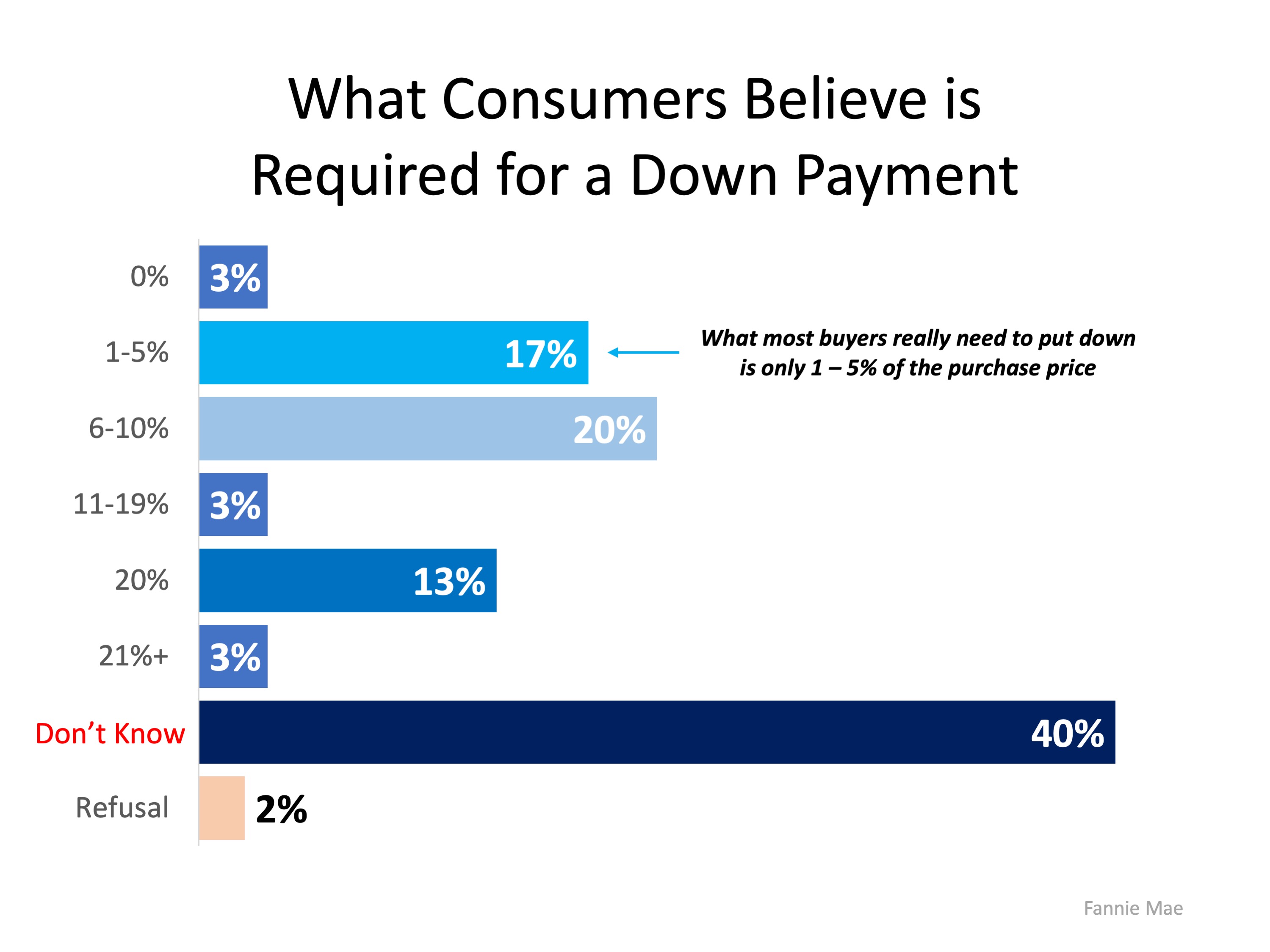

The map below shows the average tax refund Americans received last year by state: According to programs from the Federal Housing Authority, Freddie Mac, and Fannie Mae, many first-time buyers can purchase a home with as little as 3% down. Truth be told, a 20% down payment is not always required to buy a home, even though that’s a common misconception about homebuying. Veterans Affairs Loans allow many veterans to purchase a home with 0% down.

According to programs from the Federal Housing Authority, Freddie Mac, and Fannie Mae, many first-time buyers can purchase a home with as little as 3% down. Truth be told, a 20% down payment is not always required to buy a home, even though that’s a common misconception about homebuying. Veterans Affairs Loans allow many veterans to purchase a home with 0% down.

How can my tax refund help?

If you’re a first-time buyer, your tax refund may cover more of a down payment than you ever thought possible.

If you take into account the median home sale price by state, the map below shows the percentage of a 3% down payment that’s covered by the average tax refund: The darker the blue, the closer your tax refund gets you to homeownership in one of these programs. Maybe this is the year to plan ahead and put your tax refund toward a down payment on a home.

The darker the blue, the closer your tax refund gets you to homeownership in one of these programs. Maybe this is the year to plan ahead and put your tax refund toward a down payment on a home.

Bottom Line

Saving for a down payment can seem like a daunting task, but the more you know about what’s required, the more prepared you’ll be to make the best decision for you and your family. This tax season, your refund could be your key to homeownership.

|

|

|

JERRY TORRES Sr. Mortgage Loan Originator | Vision One Mortgage, Inc “THE PERFORMANCE TEAM”

#TechieLoanOriginator | #JerryTorresPro

|

![What You Need to Know About the Mortgage Process [INFOGRAPHIC] | Simplifying The Market](https://www.jerrytorres.pro/blog/wp-content/uploads/2019/10/20191011-MEM.jpg)

![A Latte a Day Keeps Homeownership Away [INFOGRAPHIC] | Simplifying The Market](https://www.jerrytorres.pro/blog/wp-content/uploads/2019/08/20190823-MEM.jpg)