The Community and Economic Impacts of a Home Sale

If you’re thinking of buying or selling a house, chances are you’re focusing on the many extraordinary ways it’ll change your life. What you may not realize is that decision impacts people’s lives far beyond your own. Home purchases and sales are significant drivers of economic activity. They have a major impact on your community and the entire U.S. economy via the multiple industries and professionals that take part in the process.

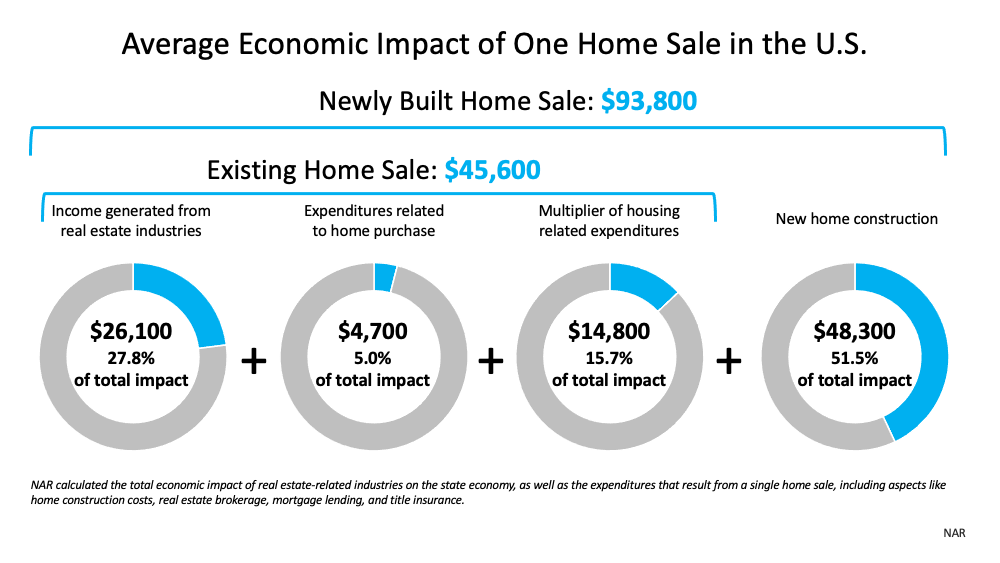

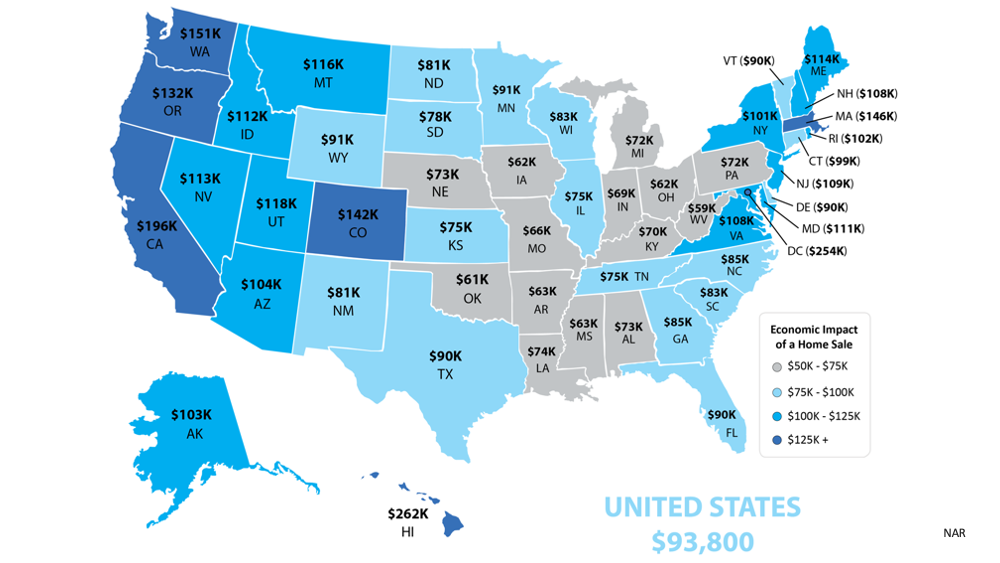

The National Association of Realtors (NAR) releases a report each year that highlights just how much economic activity a home sale generates. The chart below shows how the sale of both a newly built home and an existing home impact the economy: To dive a level deeper, NAR also provides a detailed look at how that varies state-by-state for newly-built homes (see map below):

To dive a level deeper, NAR also provides a detailed look at how that varies state-by-state for newly-built homes (see map below): As you can see, a single home sale can have a massive effect on the overall economy. Ali Wolf, Chief Economist for Zonda, talks about this in a recent article, noting there’s a significant impact at each distinct phase of the transaction:

As you can see, a single home sale can have a massive effect on the overall economy. Ali Wolf, Chief Economist for Zonda, talks about this in a recent article, noting there’s a significant impact at each distinct phase of the transaction:

“The housing market contributes to the economy in four main stages: during planning and land development, throughout the actual construction of the home, at the point of sale, and upon moving in.”

When you buy or sell a home, you’re leaving a lasting impression on the community at large in addition to fulfilling your own needs. That’s because each stage of the process involves numerous contractors, specialists, lawyers, town and city officials, and so many other professionals. Every individual you work with, from your trusted real estate advisor to the architects who design new homes, has their own team of professionals involved behind the scenes.

Bottom Line

Homebuyers and sellers are economic drivers in their community and beyond. If you’re thinking of buying or selling, let’s connect today to start the process. It won’t just change your life; it’ll make a powerful impact on our entire community.

|

|

|

JERRY TORRES’ Sr. Mortgage Loan Originator

Team@JerryTorres.Pro #TechieLoanOriginator | #JerryTorresPro

Prime & NON-Prime Home Loans | Bank Statement Loans | ITIN | HELOCs |

![Waiting To Buy a Home Could Cost You [INFOGRAPHIC] | Simplifying The Market](https://www.jerrytorres.pro/blog/wp-content/uploads/2021/07/20210723-MEM-1.png)

![Pop Quiz: Can You Define These Key Terms in Today’s Housing Market? [INFOGRAPHIC] | Simplifying The Market](https://www.jerrytorres.pro/blog/wp-content/uploads/2021/07/20210723-MEM.png)